Contrary to popular belief, the market works! The trick is knowing how to win the game!

Here are some facts to consider:

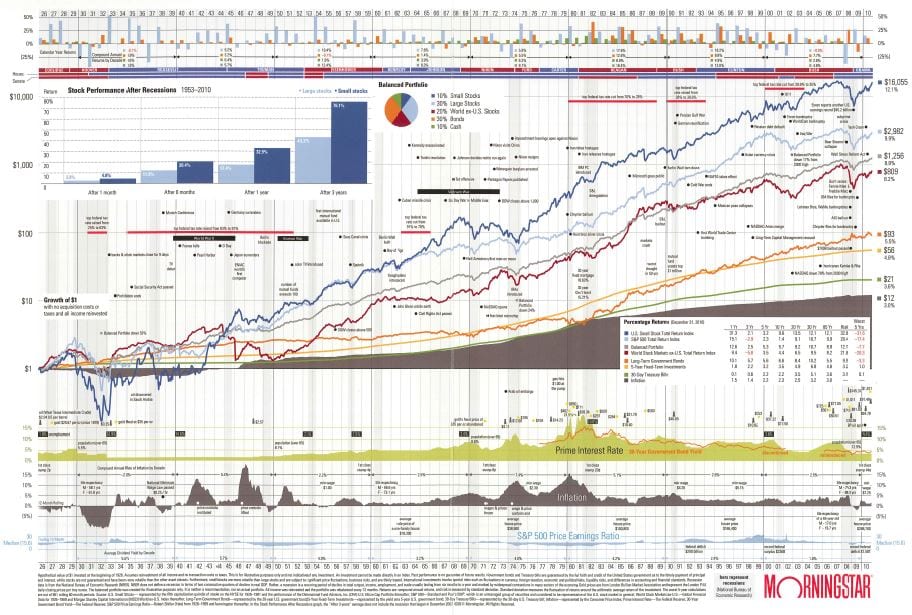

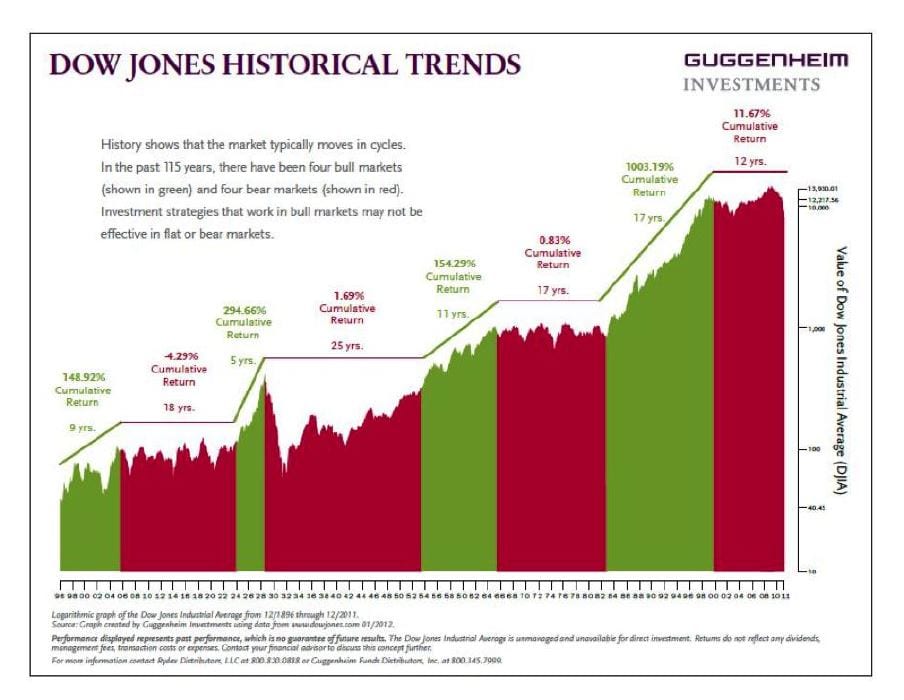

The market has shown steady long-term growth

The stock market is often volatile and unpredictable

Consistent returns are almost impossible to time or predict

There are winners and losers in the Market

Short-term investing produces higher risks, but not always higher rewards!

Emotional decisions usually produce undesirable results

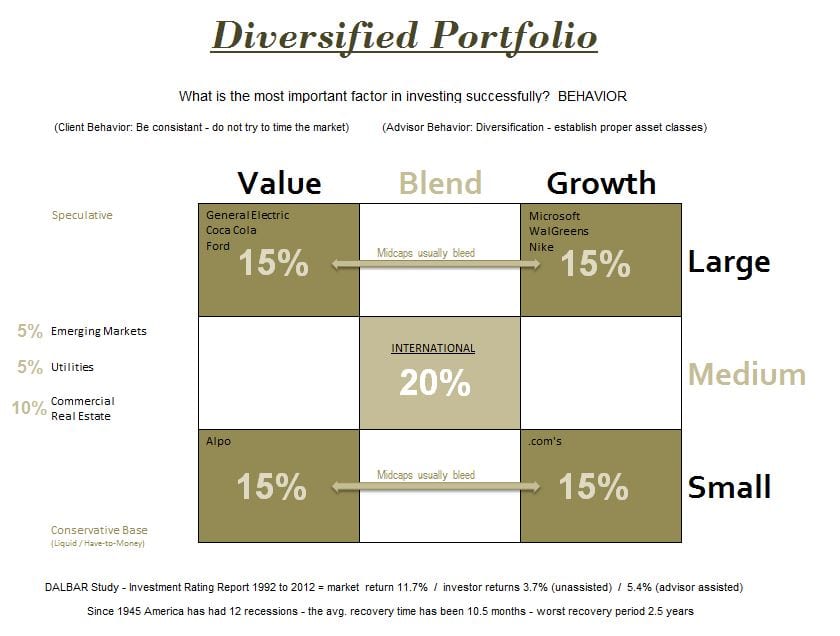

Winning consistently in the Market takes several things; discipline, a solid investment strategy, access to historical performance, an understanding of asset allocation, dollar cost averaging, and then having the patience and the perspective to capitalize on the correct market opportunities. One of the biggest factors to finding and capitalizing on these opportunities continues to be who you hire to manage your money.

Play the Most Popular FREE Stock Market Game on the Web!

Sometimes the best way to learn something is to do it! Click on the icon above (How the Market Works) and play the stock market game without investing any of your hard-earned money.

"One of the funny things about the stock market is that every time one person buys, another sells, and both think they are the astute investors!"

William Feather

A Good Reputation is a Must

Ask a trusted advisor for a referral. They are not going to put their reputation on the line for someone they don’t completely trust. Then, do a little research; What kids of reviews do they have? How long have they been is business? What kinds of testimonials do they have and who made them?

Finding the Right Advisor!

Knowledge is power! Every good Investment Advisor I have ever known analyzes the risk in a portfolio and wants to increase returns… but what makes them better than the next guy? There are a few things you need to know to help you find the right Advisor.

The Market works!

So how long has your Financial Advisor been in business and how successful have they been? Ask to talk to a few of their clients. They may hand-pick them, but at least you will know how they communicate and if they follow through. Ask things like; What types of returns do they average? Average cost to manage their money? Do they have annual reviews? Etc…

Next, Discuss is the Fees!

According to the DalBar Studies over the past 30 years the stock market has averaged between 11% and 12%. However, individual investors have made only 3.5% to 4% over the same period and if they had an advisor the return increased to almost 6%. Most advisors charge at least 1% to manage money, but you need to know how much your being charged with all fees included… it should be somewhere between 2% and 2.5%.

The Market is a Big Place!

So how does your advisor pick the investments you are going to buy? What is their system? How are they limiting your risk? Is your Advisor buying the same investments you are buying? Does your Advisor even invest in the market? Ask them a few questions, this information will tell you a lot.

Limiting Market Losses Combines Many Disciplines

First, historical performance on the information is the real challenge. These things will help you to find the right Financial Advisor! can help us to see trends and to learn from the past Things like diversification, dollar-cost averaging, and our risk tolerance can help to spread the risk and decrease volatility. The stock market works, but consistently capitalizing on this information is the real challenge! These things will help you to find the right Financial Advisor!

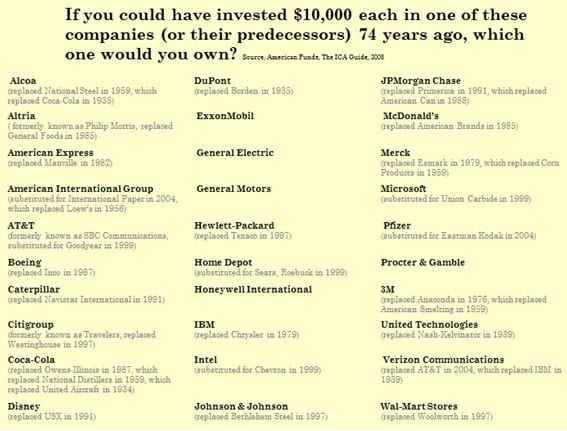

Predicting the Market

The stock market is random and unpredictable. However, there are some who believe they can master anything, and to those of you who are wired this way, we have provided the following exercise or test below. The stock market is random…the following exercise or test below.

Test Yourself

If you could have invested $10,000 in the stock market in 1933, and you could choose one of the companies listed here, which one would you choose?

They say hindsight is 20/20 so you are getting the benefit of knowing most of these companies and their track record over the past 85 years!

Your Financial Plan has multiple components, all of which are important for you to become financially self-reliant. Budgeting and Debt Elimination are the catalysts of any good financial plan. Emergency Savings together with long-term and short-term savings add fuel to the fire. Risk Management then helps to protect you and your assets/liabilities from unforeseen problems. This allows you to turn your liabilities into assets, giving you the ability to use the payment savings to grow your retirement nest egg.

While all of the things mentioned are important to building your Financial Map, the acquisition of life and disability insurance allows your dreams to be realized even if there is a future catastrophic event, that would otherwise have compromised your plans. It’s a balancing act, where each of the blocks you have carefully stacked could come toppling down without the support of the others. Ask an M3 Wealth Financial Cartographer or guide how to build a solid self-completing Financial Map!

Schedule and Complete your COMPLIMENTARY “Retirement Planning Appointment”

and get… Patrick Kelly’s best-selling book; Stress-Free Retirement as our FREE gift!

Important: The information contained on this website is provided for informational purposes only. All articles, charts, brands, logos, names, or other information used is the sole property of the parties cited or referenced. The information on this website should not be construed as investment, legal, or tax advice. M3 Wealth is in no way attempting to provide investment advice. Any use of this information is the direct responsibility of the reading party and should be reviewed and discussed with their financial advisor, attorney, or CPA prior to implementation and/or use. The information contained on this website cannot be used, altered, or distributed, without the express written consent of M3 Wealth.