Understanding the impact of the things you buy is critically important! We want everything now and we have been taught that we owe it to ourselves, after all we deserve the very best!

Our grandparents saved until they had the cash to pay for these items, but with easy access to credit most of us buy what we want, and we seldom wait. We have been taught to focus on interest rates instead of loan terms and the "true cost" of the things we buy. Consequently, the average American walks away from more than $1,000,000 in their lifetime by avoiding or ignoring the true cost of their debt.

In essence, we rob ourselves by spending our retirement early, instead of measuring the impact of these daily decisions. We spend the dollars we could have saved and the interest we could have compounded, because we can’t see retirement today.

Installment interest is generally paid on term loans for things like a car, a house, a boat or and recreational vehicle. If we owe $10,000 on an installment loan and we pay an extra $1,000 to principal it may shorten the term of the loan from 60 months to 50 months. However, the payment stays the same and if we default on the loan we can lose the item, even though we paid extra payments.

Revolving Interest

Revolving interest is generally paid on revolving loans for things like credit cards, department store cards, or a home equity line of credit. If we owe $10,000 on a revolving loan and we pay an extra $1,000 to the principal it lowers both the principal and the payment. So, if we continue to pay the same payments, it will pay off the principal much sooner because the interest compounds in our favor. Every payment we make after the lump sum payment of $1,000 lowers our payment every month, and the interest is reduced much quicker than the installment loan.

Buying a Car

Do your homework before you start looking for a specific car. Develop a budget and research cars online to find the right make model and year.

Don’t get hung up on the new car smell! Buying a great used car can save you thousands of dollars.

Use online tools like TrueCar or Carfax to establish an average price and service record for the car or cars you have chosen.

Next, gather up your taxes for the last couple of years, your last two pay stubs, and talk to your bank or credit union about the rate and terms. Have your lender prequalify you for an amount that matches your budget.

It’s time to find a car. Look online or head to a dealership to find the right car for you. Don’t fall in love, stick to your budget. If the dealer can’t beat your rate stick with your pre-approved deal.

The sticker price is not the sale price, negotiate to get the best deal. Rely on the research you’ve done and do not let anyone pressure you.

Do your homework before you start looking for a specific house. Save for a down-payment, develop a budget, and research houses online to find the right features and amenities.

Research the schools in the area, access to shopping, busy streets, and neighborhoods.

Use online tools like Zillow, Realtor.com, or Trulia to view homes and local pricing.

Next, gather up your taxes for the last couple of years, your last two pay stubs, and talk to your bank or credit union about the rates and terms. If you need help, you can talk to our Mortgage Specialist listed below.

Have your lender prequalify you for an amount that matches your budget.

It’s time to find a House. Don’t overspend, stick to your budget. Your mortgage payment with taxes and insurance should be 25% to 30% of your NET or take-home pay.

Find a good realtor in the area to help you negotiate the best deal. Rely on the research you’ve done and do not let anyone pressure you.

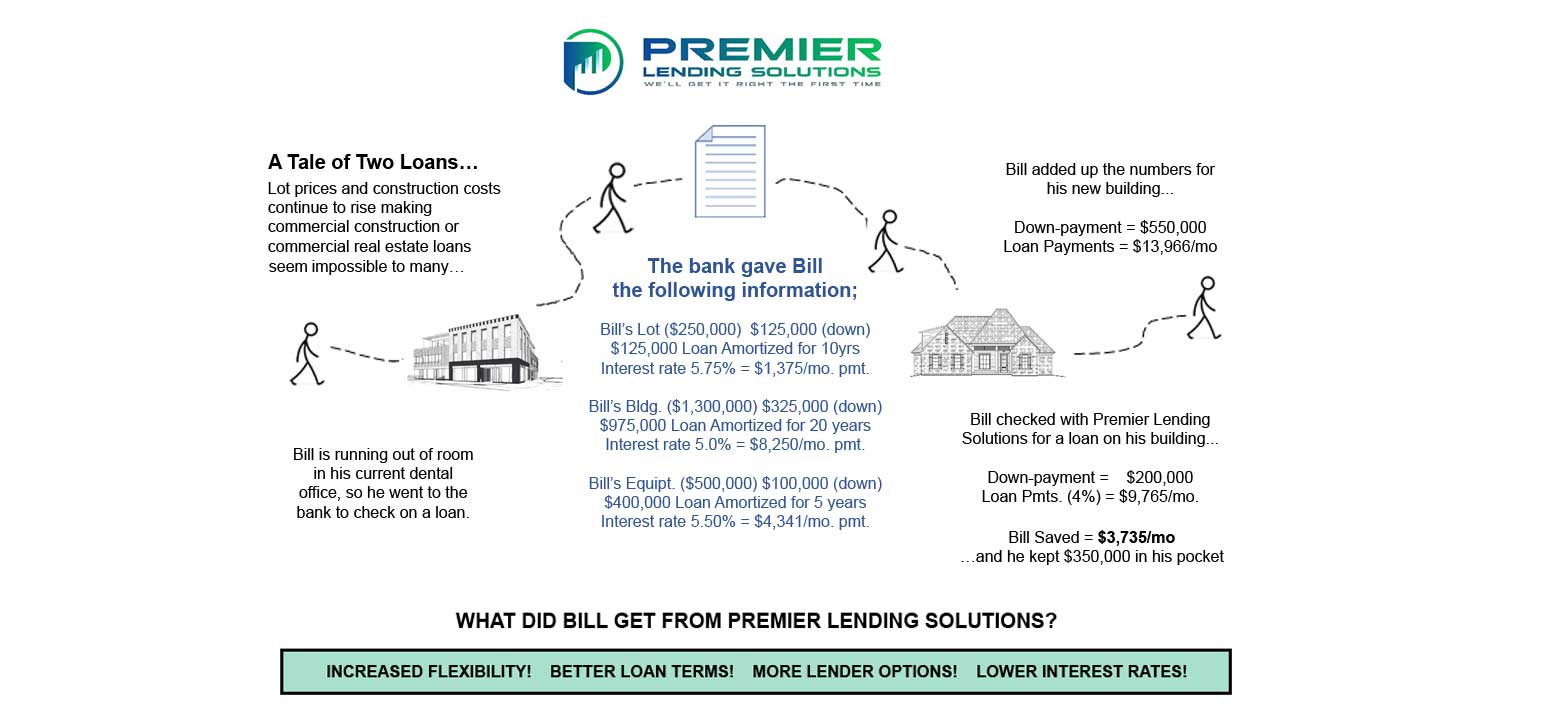

Premier Lending Solutions has built long-term relationships with several local/national banks and specialty lenders. We can help you to find and secure the best loan for your business refinance, construction to permanent real estate loan, lot loan, SBA or conventional loan, specialty loan, equipment loan, and even working capital.

Many of our clients have used Premier Lending Solutions to negotiate and secure a loan that was .5% to 1.0% lower than the rates they were being quoted by their own bank. In addition, we help our clients to manage the lending process, negotiate with the lender, overcome common obstacles, and we are able to help them properly structure their debt (saving them tens of thousands of dollars or more).

Business Loan Documentation

Last 3 Years Individual Tax Returns (all partners owning more than 10%)

Personal Financial Statement (updated in past 90 days)

Last 3 Years Business Tax Returns

YTD P&L and Balance Sheets

Year-End P&L and Balance Sheets (prior 2 years)

5 Year Proforma

Business Debt Schedule (updated in past 90 days)

Business Equipment List (updated in past 90 days)

Accounts Receivable Aging (updated in past 90 days)

Entity Documents and TIN Documents

Project Summary (detailing sources and uses of funds)

Premier Lending Solutions has been providing loans to America’s farmers for the past two decades. Our Agricultural Department has developed both local and national lending partnerships to assist you with your full-time and part-time farm needs! Let us help you find and secure the best loan for your farm or ranch.

Many of our Ag customers have used Premier Lending Solutions to negotiate and secure loans that were .5% to 1.0% lower than the rates they were being offered elsewhere. Let us help you to refinance or expend your existing farm or ranching operation.

Business Loan Documentation

Funding Request (detailing sources and uses of funds)

Ag/Farm Loan Application

Last 3 Years Individual Tax Returns (all partners owning more than 10%)

Personal Financial Statement (updated in past 90 days)

Schedule and Complete your COMPLIMENTARY “Retirement Planning Appointment”

and get… Patrick Kelly’s best-selling book; Stress-Free Retirement as our FREE gift!

Important: The information contained on this website is provided for informational purposes only. All articles, charts, brands, logos, names, or other information used is the sole property of the parties cited or referenced. The information on this website should not be construed as investment, legal, or tax advice. M3 Wealth is in no way attempting to provide investment advice. Any use of this information is the direct responsibility of the reading party and should be reviewed and discussed with their financial advisor, attorney, or CPA prior to implementation and/or use. The information contained on this website cannot be used, altered, or distributed, without the express written consent of M3 Wealth.